Published July 3-26, 2021

1

Overview

Over the past year, I have written extensively about two marketing ideas: Velvet Rope Marketing (VRM) to provide differentiated experiences to Best Customers and Microns to engage and reactivate Rest Customers. I have also done over a hundred presentations to marketers in India and South-East Asia on these ideas. During this period, my own thinking has evolved, and I have realised that there is a need to provide a simplified view of this new marketing framework. This is what we will discuss in this long series.

The topics I will cover are:

- How marketers have erred by focusing excessively on acquisition of future customers and not enough on attention from their present customers and thus created past customers

- The disruption coming because of Google’s decision on third-party cookies and Apple’s new privacy features, and their compounding impact on marketing

- The 90:10 adtech:martech skew, as shown in a survey of India’s adtech and martech spends

- The broken state of marketing today: how marketers ignore existing customers…

- …and how customers have been trained to ignore marketing messages

- …thus creating a chasm, and sending marketers into the “doom loop” of a perpetual acquisition arms race

- Marketing’s Power Law: 20% of customers generate 60% of revenues and 200% of profits

- How marketers are leaving money on the table by not understanding the fact that “all customers (and attention) are not equal”

- How marketers can win back their customers’ attention – by making it the new acquisition

- Building the attention stack, starting with CDP, CLV and BCG

- How marketers can imagine the ideal business endgame: a profipoly

- Rethinking the marketing core with teams for Best, Rest and Next customers

- The big idea: to get customers to pay attention, pay for attention; think Microns and Mu

- How to make it happen: why the modern marketer needs a quartet of ‘robots’: ABC, C2E2, M3 and AMB

- Why it will take a constellation of companies to bring this new world to life

- The choice CEOs and marketers face: growing profits for Google-Facebook or their own

This is a journey with many deteours. Not all of them may be initially obvious, but look at is taking the scenic route! There’s a lot to learn and understand. And at the end, I will provide a summary of the key points to show the path to simplifying marketing and starting the journey to higher profits. Off we go!

2

Marketers’ Mistake

In the pre-digital world, it was very difficult and expensive for brands to build 1:1 relationships with customers. Data collection was hard and communication had to be via post. So, few B2C companies did that. The Internet changed everything because it gave a digital identity to every customer: an email address and/or a mobile number. Now, it became possible to send messages either as broadcasts or targeted individually. This also incentivised marketers to collect data about customers. The more data one had, the more customised the messaging could be. This has led to the rise of martech – tools and technologies to enable engagement with existing customers. The endgame: omnichannel personalisation.

This contrasts with adtech where there is no personally identifiable information (PII). That is why other identifiers like cookies and device IDs are needed to connect activity across sites and sessions for non-logged in users. Adtech thus is perfect for new customer acquisition. In the early days of the Internet, media platforms served as the intermediaries between brands and their future customers. As websites proliferated, the gatekeepers changed to the search engines and then the social media platforms which garnered the attention. This shifted the balance of power to companies like Google and Facebook, who in turn grew their footprint and data hoard. Cut to today, and the duo have amassed massive power to the extent that almost 90% of the incremental ad spend goes to them.

This is where I believe marketers made a big and costly mistake. Seduced by the ease of spending on Google and Facebook, and the excitement of continuously acquiring new customers, they missed deepening relationships with existing customers. It is not just marketers but even CEOs who are at fault. The question that gets asked is: how many new customers did we acquire? There is little discussion about retention and revenue expansion from existing customers. (This is true for B2C and B2B brands.) In a competitive market, the focus shifts to landgrab and leads to an arms race of spending investor money or retained profits to show perpetual growth of website traffic or app installs. The rise of ad revenues of Google and Facebook testify to the marketers’ folly.

By not building deep relationships with existing customers and by bombarding them with irrelevant messages, marketers have trained their customers to ignore their communications, thus reducing the efficacy of the only method of bringing existing customers back to their website or app for transactions. Once customers start ignoring the messages, the marketer has little or no choice but to spend 10X more on re-acquiring that same customer via the tech giants. With everyone doing the same, the only winners are the attention sellers (Google and Facebook), who in turn create even more powerful data hoses by giving consumers even more free utilities. The irony is that as marketers did not pay attention to their customer needs, they are paying even more dearly to the attention intermediaries to reach their own ex-customers.

This has been the big blunder that marketers made: they did not value the attention of their customers. Instead of building a hotline, they cut the line. Now, the digital people are fighting back. They want their privacy. This is forcing the tech giants and device makers to act, and changing the rules of marketing as we know it. It is also creating a chance for marketers to correct their past mistake of ignoring their existing customers. Marketing is thus getting disrupted and marketers have an opportunity to simplify it.

3

Data and Disruption

To quote Seth Godin, “Marketing is a contest for people’s attention.” Attention is upstream to actions and transactions. Marketers lost the attention contest to Google and Facebook. The privacy pushback is giving them yet another opportunity to get back into the game. Let’s begin by taking a look at how the push for privacy threatens the status quo of marketing.

With the rise of digital, marketers today have an array of targeting tools to keep up with the omnichannel customer. These martech platforms have become feature-rich and are capable of providing personalisation to a degree that was not possible earlier. Every action of the customer across all engagement and transaction channels can now be captured, ingested into a database and then be used to provide a better journey for the customer at every stage of the interaction to push faster for the elusive next transaction. AI-ML can automate many aspects of the orchestration.

However, in this data-rich world, the trees are a barrier to understanding of the forest. The means are taking over and the ends are getting forgotten. The tyranny of the daily campaign and then analysing opens, clicks, installs, uninstalls is heightening complexity to unprecedented levels. Dashboards give a huge array of information making it almost impossible to understand what is important and what should the marketer do next. And when marketers are in doubt, the result is yet another broadcast campaign.

Now look at the situation from the customer’s angle. A flood of messages – emails, SMSes, push notifications, in-app messages, browser notifications, and of course the eerie retargeting on different based on our activity on the brand’s properties. It makes the customer feel they are being snooped on continuously – which is of course true. In the digital world, no action is secret or goes untracked. Everything we as customers do is stored in databases forever – all going to build our profiles, compare us with others like us, and then begin the game of persuasion for the next best action.

The backlash has already begun. Privacy has become the central theme across the operating systems that dominate our digital lives – Apple’s iOS and Android. Cookies are set to be banished, email trackers are being stopped, and a wall is being constructed between brands and consumers. Without first-party data and explicit permissions, personalised engagement will become almost impossible. This rapid change is creating a new world for advertisers (for acquisition of new customers) and marketers (for retention and growth of existing customers).

Martech tools complexity and digital data disruption are here to stay. In this new era, what will change and what will stay constant? What should marketers do? Is it possible to cut through the clutter and think from first principles? Before we answer these questions, let us take a look at some of the recent changes that will leave a lasting impact on adtech and martech.

4

Cookies

The cookieless future. That has become the new buzzword as Google decided to phase out third-party (3P) cookies and Apple to end the use of device identifiers for advertisers (IDFA). Even though Google recently delayed the decision by almost two years to late 2023, marketers need to start planning now for a future without 3P cookies. As Jerry Daykin tweeted: “Forward thinking marketers still need to be building future-ready data & marketing approaches that reflect shifting consumer privacy expectations.”

Let’s begin with a brief explainer on first-party and third-party cookies, and IDFA.

Cookies: From Wikipedia: “Cookies are small blocks of data created by a web server while a user is browsing a website and placed on the user’s computer or other device by the user’s web browser. Cookies are placed on the device used to access a website, and more than one cookie may be placed on a user’s device during a session. Cookies serve useful and sometimes essential functions on the web. They enable web servers to store stateful information (such as items added in the shopping cart in an online store) on the user’s device or to track the user’s browsing activity (including clicking particular buttons, logging in, or recording which pages were visited in the past). They can also be used to save for subsequent use information that the user previously entered into form fields, such as names, addresses, passwords, and payment card numbers.”

First-party cookies: From CookiePro: “First-party cookies are directly stored by the website (or domain) you visit. These cookies allow website owners to collect analytics data, remember language settings, and perform other useful functions that provide a good user experience. An example of a first-party cookie is when a user signs into an ecommerce website, like Amazon. The web browser will send a request in a process that provides the highest level of trust that the user is directly interacting with Amazon. The web browser saves this data file to the user’s computer, under the “amazon.com” domain. If first-party cookies were blocked, a user would have to sign-in every time they visited, and they wouldn’t be able to purchase multiple items while shopping online because the cart would reset after every item that was added.”

Third-party cookies: From Cookie Script: “Third-party cookies are cookies that are set by a website other than the one you are currently on. For example, you can have a “Like” button on your website which will store a cookie on a visitor’s computer, that cookie can later be accessed by Facebook to identify visitors and see which websites they visited. Another example would be an advertising service (ex: Google Ads) which also creates a third-party cookie to monitor which websites were visited by each user. This is the main technology used to show you products that you previously searched for on a completely different website.”

To complete the picture, here is ClearCode on second-party cookies. “Second-party cookies are cookies that are transferred from one company (the one that created first-party cookies) to another company via some sort of data partnership. For example, an airline could sell its first-party cookies (and other first-party data such as names, email addresses, etc.) to a trusted hotel chain to use for ad targeting, which would mean the cookies become classed as second-party.”

More from Ionos on third-party cookies: “Third-party cookies are mostly used for web analytic purposes. This can happen if your web browser loads an advertisement or a so-called targeting pixel that is not hosted on the server of the visited website. Your web browser generates an additional cookie, the third-party cookie, because it is not assigned to the server of the website, but to that of the advertiser. Nevertheless, this third party cookie reads all the information that the first-party cookie notes anyway – and sometimes even more. Because web analysts are primarily interested in user behavior, the third-party cookie usually documents the page history on a website. However, this cookie often gains really valuable data only when it “recognizes” you on another website. Since your web browser communicates again with the same ad server, it can trace your path on the internet, and not only that: your behavior on the web reveals a lot about your interests and your consumer behavior. This creates a user profile that enables targeted and personalized advertising.”

Cookie Script once again: “Let’s say earlier in the week you looked up some vacation rentals in Cancun. You browsed a few websites, admired the photos of the sunsets and sandy beaches, but ultimately decided to wait another year before planning your vacation. A few days go by and suddenly it seems like you are seeing ads for Cancun vacations on many of the websites you visit. Is it a mere coincidence? Not really. The reason you are now seeing these ads on vacationing in Cancun is that your web browser stored a third-party cookie and is using this information to send you targeted advertisements.”

5

IDFA

Apple’s world doesn’t have cookies. It has an equivalent called Identifier for Advertisers (IDFA).

From Adjust: “The IDFA is a random device identifier assigned by Apple to a user’s device. Advertisers use this to track data so they can deliver customized advertising. The IDFA is used for tracking and identifying a user (without revealing personal information). The data can then be used to discover information such as which in-app events a user triggers. The IDFA can also identify when users interact with a mobile advertising campaign, provided the channel offers IDFA tracking and the advertiser tracks users who interact with as successfully. If this occurs, the IDFA can identify whether specific users click an advert for payment and attribution purposes.”

More from Mozilla’s blog: “IDFA…is a random identification number, similar to a cookie, that tracks what you do in apps on your device. Each iPhone comes equipped with its own unique ID attached, which allows advertisers to track your interactions from what you click on, to what apps you install, to what videos you watch. The New York Times did an investigation last year that found data brokers were able to link these IDs with other information like name, location or email address to make complex user profiles, which isn’t great for your privacy. If you have an iPhone and didn’t turn this identifier off, then yes. It was possible to turn it off before, but you had to manually go in and do it yourself. Almost 70% of people did not turn off the tracker, according to a 2020 study by the analytics platform, Singular.”

Invoca: “You can think of an IDFA as something like a cookie that is tied to devices instead of browsers, in that it enables an advertiser to get notified when a user of a phone has taken an action like clicking on their ad in a browser and then installing, using, or interacting with ads in their app. This identifier is used in non-browser apps, which never had support for cookies. IDFAs only provide advertisers data in aggregate and no individually identifiable data is available.”

Cookies and IDFA are the trackers that power the world of digital advertising. And then in one fell swoop, Google decided to do away with third-party cookies and Apple made big changes to IDFA.

6

Changes

In January 2020, Google announced it would phase out support for third-party cookies in Chrome in 2 years. From the announcement: “Users are demanding greater privacy–including transparency, choice and control over how their data is used–and it’s clear the web ecosystem needs to evolve to meet these increasing demands. Some browsers have reacted to these concerns by blocking third-party cookies, but we believe this has unintended consequences that can negatively impact both users and the web ecosystem. By undermining the business model of many ad-supported websites, blunt approaches to cookies encourage the use of opaque techniques such as fingerprinting (an invasive workaround to replace cookies), which can actually reduce user privacy and control.”

From a recent Google post advocating a more privacy-first web: “Developing strong relationships with customers has always been critical for brands to build a successful business, and this becomes even more vital in a privacy-first world. We will continue to support first-party relationships on our ad platforms for partners, in which they have direct connections with their own customers. And we’ll deepen our support for solutions that build on these direct relationships between consumers and the brands and publishers they engage with.”

Google’s alternative to third-party cookies is Federated Learning of Cohorts (FLoC).

Apple’s iOS 14 update gave primacy to privacy, and allowed users to block IDFA at the app level. From GamesBeat: “With the new version of iOS, every app has to ask you upfront whether it’s OK to share your data with third parties. If you opt out, then advertisers will lose access to IDFA data and their ability to track you when you download games or make in-app purchases. Before this change, advertisers could freely track your mobile habits and precisely target you with offers that could generate a lot of revenue for the advertiser, whether it was a mobile game company or a travel app maker.” Basically, the opt-out became an opt-in.

And then came the recent announcement that iOS 15 would put a stop to email tracking pixels. From MacRumours: “Tracking when you’ve opened up an email and what you’ve read is something that many companies and advertisers rely on for their marketing efforts, plus there are email clients out there designed to let users know when the emails they’ve sent have been opened up. Much of this tracking is facilitated by remote images that load when viewing an email, and some of it is even sneakier, with advertisers using invisible tracking pixels. Tracking pixels are hidden graphics that you might not see in an email, but your email client loads them, allowing senders to gather data from you. Senders can see that you’ve opened an email get other information, such as your IP address.”

The demise of third-party cookies, the blocking of IDFA and the end of email tracking pixels – all herald a very different future for advertisers and marketers. And it is in this future that marketers need to go back to basics and create a simple model of their customers and build engagement with them. But before we get to that, let us understand the impact of all these changes.

7

Impact – 1

All the recent changes are going to dramatically change the relationships between brands and their present and future customers. There has been a lot of commentary about the impact of these changes.

The Drum: “Third-party cookies have been integral for digital marketing over the last 10 years and their reach covers everything from audience targeting to behaviour tracking to remarketing and more. However, with searches for “online privacy” at an all-time high and this being a key concern for people around the world, the old method of collecting behavioural data as we browse needs to change and that’s why Google will be depreciating cookie…For marketers, the key challenge will be to strike the right balance between having the necessary privacy and security in place while delivering a customised user experience.”

Mark Bergen: “Mobile advertising inside apps is a sizable business, and Apple’s move has the potential to gut the sector. Companies that rely on these ads for sales or growth have warned investors of coming damage, particularly as Apple’s iOS mobile operating system typically brings in more money for developers than Android. Then there are the wealth of ad agencies, ad-tech firms and data brokers that thrive on web cookies. Bank of America research estimated Apple’s change could shave as much as 3% off Facebook’s revenue. Google’s upcoming move offers less certainty. Executives at Criteo SA, an ad re-targeting firm, told investors they were working with Google to prepare for FLoC, but weren’t yet sure of the financial impact.”

ET Brand Equity: “Marketers need to find alternative ways to increase digital fingerprints across different devices, since the role of cookies is gradually decreasing. Neil Patel, entrepreneur, angel investor and digital marketing expert, said that companies are looking for solutions to get enough information about users even without cookies, using customer data platforms…He said, “Customer data platforms are great because you can learn all about your customers in one platform. It is similar in many aspects to CRM, but more so for customer data.””

Dr. Augustine Fou in Forbes: “The moves by Google and Apple increase privacy for consumers. That’s a good thing, after years of wanton data collection by ad tech companies, violating consumers’ privacy without their knowledge, consent or recourse…Ad tech companies are arguing that the loss of 3P cookies is a bad thing because that means the loss of the ability to target ads down to the level of the individual. What they are really saying is that it impairs their ability to make revenue selling services based on 3P cookies, like audience segments, behavioral targeting, etc. Marketers should consider whether targeting down to the level of the individual is actually worth it or actually works in the first place, given how poor the data quality is… When all of the useless and harmful things built on 3P cookies go away, the associated costs go down and the effective business outcomes from digital marketing go back up. More specifically, when advertisers buy ads from real publishers with real human audiences, they will get better outcomes than hyper targeted ads shown on millions of long tail sites to bots, pretending to be various audiences.”

WSJ on FLoC: “The idea behind FLoC, one of a handful of advertiser tools that Google is proposing, is to allow advertisers to request and use pools of online identities with common characteristics, rather than individuals. The underlying data will come from browsers that use machine learning to develop cohorts based in part on the sites that individuals visit. Advertisers will receive an identifier for a cohort rather than for the individuals within it.”

8

Impact – 2

IRI marketing strategy and effectiveness director Carl Carter quoted in Marketing Week: “Brands need to employ a wider range of data sources and technology to discover consumers’ interests and ensure advertising is cost-effective and efficient, especially when reach is vital due to lower conversion rates in sectors like FMCG. Ultimately privacy and trust are more important going forward and brands have to pay attention to that. The industry is moving towards a ‘first-party identity resolution’ approach to tracking users across touchpoints, which is centred on trust because the data comes from consumer permissions. Over time you can build more quality customer relationships, and can target people more effectively and recommend products that make a difference to their lives. When it comes to marketing effectiveness, it also means closed-loop attribution so you know who has seen your ad and if they have purchased. This should lead to a better return from your ad spend.”

iapp: “The general alignment between Google’s and Apple’s approaches and the synched timing is no accident. Both Apple and Google have issued statements that these changes are driven by consumer demands for privacy and control over their personal information.”

Nishant Desai of Xaxis in MarketingDive: “For advertisers and their partners, third-party cookies today are really just proxies for consumers. We use the data those cookies provide to find people in choice audience segments with messages we hope will engage them. Without that data, marketers will have to find new ways to reach consumers and prospects. We’re being given the push we need to more directly interact with individuals and build one-on-one relationships, which will in turn force us to be more open about how we’re connecting… A new wealth of more direct data will serve several other useful purposes as well. It will make ads better targeted and more effective. It will aid in customer relations, market research and product ideation. One top marketing executive for a major hotel and resort chain recently spoke of asking customers to specify their preferences, then delighting them by deeply customizing their stays to cement their desire to visit the properties again.”

More from MarketingDive: “The email-related features will likely limit the ability of email marketers to collect information about consumers or know when they open emails — a key way to measure the effectiveness of email marketing campaigns…Apple’s previous privacy changes and Google’s deprecation of cookies has led marketers to focus on first-party data. Increasingly, brands use content and e-commerce plays on their own websites to acquire email addresses that can be used for future marketing efforts. Now, as Apple tightens privacy around personal email addresses, the company is potentially limiting the efficacy of these first-party data plays, throwing a new wrench into marketers’ plans as they work to engage online consumers, a segment that continues to grow more important to many businesses.”

Matthew Dunn: “I think the most effective framework for decisions is to treat ‘pixelgeddon’ as a done deal…As a direct “push” channel, email can’t be attention parasitic for long. An email marketer is responsible for the content as a whole — the content-of-interest and the content-that-prompts-action. Because email marketers have control of their audience, in other words, their primary ability to provide content isn’t affected by the broad shift to more privacy. We may be losing one of the secondary measures — the fastest, most immediate feedback loop that was available, aka pixels. But not the primary permission and address, and ability to deliver content at incredibly low cost.” More: “I could see message platforms becoming a genuine alternative to email, and I find myself wondering if Pixelgeddon is just a feint to start moving that direction. Mess with email visibly and consumers would complain; mess with the already-invisible pixel and they’re cheering you on. Meanwhile, that messy, free-range channel (email) is just a little bit weaker as a marketing channel. If email is less measurable, and some new, high-priority-interrupt channel were more measurable and interactive…what, as a marketer, would you do?”

A few more articles detail the impact of Apple’s privacy moves on email marketing:

- Ask the Expert: How Apple’s Goodbye to Tracking Pixels will Affect Email Marketing

- 13 ways email marketers should adapt to Apple’s Mail Privacy Protection

- Apple Mail’s MPP Announcement Not a Deliverability Concern (Yet)

9

Impact – 3

Technology Review: “Third-party cookies are like Cretaceous dinosaurs. They’re munching away on consumers’ data while asteroids lobbed by Google, Mozilla, Apple, and others are on the brink of obliterating the current marketing ecosystem. Google is planning to phase out these online tracking tools by 2022. For its part, Apple plans to make its mobile device ID—known as identifier for advertisers, or IDFA—opt-in only: a move that will prevent cross-application tracking of site visitors. Their plans are only two examples of a far broader pivot toward consumer privacy that’s also been manifested in expansive pro-privacy laws such as the European Union’s General Data Protection Regulation and the California Consumer Privacy Act… “Brands must now shift the focus to first-party data strategies to effectively personalize experiences across the customer journey,” says Amit Ahuja, vice president for Experience Cloud product and strategy at Adobe…Companies need to maximize the value of first-party data: the data collected from their own domains about customers.”

Ravi Ganesh & Lloyd Mathias: “The end of browser-based third-party cookies also means that campaign planning, targeting, optimization and measurement are affected. The move signifies the death of re-targeting and lookalike marketing as practised today. Cost-per- impression-based buying will transition to cost-per-click/engagement-based buying. Walled gardens such as Google will only provide attribution within their publishing domain. Businesses need to evolve mechanisms to measure their marketing campaigns to be able to determine omni-channel effectiveness. With less than eight months left for the purge of third-party cookies and a rapidly evolving regulatory framework, businesses need to be ready to implement privacy-by-design in their marketing efforts. A sharp focus on first-party data and on contextual advertising is imminent. Time is running out and many businesses have yet to wake up to this reality.”

Ron Jacobs: “First-party data is relevant and accurate because it provides brands with data about their existing prospects and customers, and allows a marketer to create highly personalized experiences. As many as 80% of marketers plan to increase their use of internal first-party data over the 12 months…When people have actively given information to a marketer to use, the consent is clear enough — consumers expect it will be used to make ads and personalization contextually better. But consent is important. Look at what Apple is doing: Instead of just having mobile ad IDs tracking you, you have to opt in…First-party data is easily applied to email. But the digital display guys aren’t talking to the email and direct mail people — they’re on their own islands. People have to collaborate.”

AdExchanger: “CDP data is unified at the person-level, using PII. Pseudonymous IDs can be attached to this profile, of course, but there has to be a profile in the first place. A CDP using only pseudonymous IDs is basically a DMP. To work with media in the future, CDPs will need to link PII with media IDs. Post-cookie, these media IDs may well be FLoCs and “interest groups.” That linkage shouldn’t be difficult: a person visits a site and – if they log in or have a first-party cookie ID already – the first-party ID and the users’ various interest group labels are retrieved from the browser and joined.”

10

Impact – 4

David Finkelstein in Forbes: “One solution that is currently being touted by companies big and small is look-alike audience modeling powered by machine learning. What sets look-alike audience modeling apart is that it does not rely heavily on third-party data and, instead, can enable companies to leverage their first-party data. Look-alike audience solutions leverage companies’ first-party data to create a highly accurate, scalable model of a company’s ideal target consumers. Powered by machine learning technologies, the algorithms analyze large sets of nationwide consumer data and identify those consumers who share the same characteristics as the company’s top current customers. This look-alike audience model may then be used to look for other potential customers in a third-party data ecosystem that matches the needs of that particular brand. This allows companies to progressively scale up their audiences and reach potential customers in new geographic areas.”

Martech: ““Everybody will be having to tap into first parties,” April Mullen [of Sparkpost] said. “If they weren’t using a CDP two years ago, they’ll have to now. The benefit of a CDP is that if one channel goes dark on you, it’s stitching together a lot of these complex data sets and making them usable across all your channels.” The emphasis on relationships with valued customers obviously privileges first-party data over shared third-party data. Further restrictions on data through email makes some first-party data scarce and even more valuable.”.. “In first party data relationships, privacy needs to be the standard,” Jeremy Hlavacek [of IBM Watson Advertising] said. “The way for marketers to fight back is to have first party relationships instead of having a data relationship with an advertiser.

Benedict Evans writes: “Before the internet, that meant car ads in car magazines and watch ads in the Economist. Ads were based on context, and on inferring the audience from the context. The internet gave advertisers the opposite axis – it let them show ads based on the reader instead of the page. One side-effect of this was relocation of value – you can target an Economist reader a week later on a different website… Before the internet you couldn’t choose between shops or ads, but now that’s all the same algebra – how do you reach and serve a customer? If the cookie apocalypse resets the numbers for display, that money can go to search, but it can also go to Fedex or landlords. Which lever do you pull? The entire ad privacy fight is one moving part in a debate about how you reach your customers and how you spend a total of, perhaps, $7-800bn in the USA alone each year.”

He adds in his newsletter: “Apple clearly thinks privacy is the new malware: open systems are being abused in unintended ways and it’s the platform provider’s job to stop this, just as it was for Microsoft 20 years ago. The trouble is that, unlike malware, privacy also conflicts with the way a lot of advertising has worked online for 20 years, and funds open unrestricted access to things like newspapers. Cookies are going away, but we don’t know what happens next.”

11

Execution Stayed

Google’s recent announcement that it would delay the deprecation of third-party cookies by almost two years to late 2023 brought a variety of reactions:

CNet: “The delay comes amid intensifying pressure on Silicon Valley giants to fix the internet’s privacy problem. Laws like Europe’s GDPR and the California Consumer Privacy Act (CCPA) target the data collection that Google and other companies want for fine tuning the advertisements they deliver. The ad tech industry doesn’t have forever to change course because anyone dissatisfied with Chrome’s pace has abundant alternatives…One part of Google’s rationale for pushing back its plan is that moving too fast will encourage tracking companies to use sneakier tracking methods than cookies. One such method, fingerprinting, uses trackers to gather browser configuration details, such as the version you’re using and which fonts you’ve downloaded. With enough of those details, trackers can identify you accurately…Google is working on revisions to FLOC, too.”

AdExchanger: “News of Chrome’s delay in killing off third-party cookies is a shock: Ad tech companies and publishers have been working in overdrive to transition away from third-party identifiers and to adapt to Google’s Privacy Sandbox in time for change next year. Agencies have also pressed brand clients to onboard new identity vendors and cookieless targeting technology, with a sense of urgency driven by Google’s deadline. Some in the industry may not be surprised to hear that Google is delaying the policy change. The FLEDGE trials – early tests of some Privacy Sandbox proposals – have been delayed as well, until late this year or early next. That wouldn’t leave much time for the U.K. Competition and Markets Authority (CMA) to approve changes and for developers to adopt new privacy technology…Third-party cookies won’t disappear like a flip of the switch. Instead, think of it as a slow dimmer.”

Gizmodo: “While nobody’s a fan of the creepy tech that tracks and targets us across the web, Google’s initial plans to kill them off received a fair bit of flack for a few reasons. First, privacy advocates have pointed out time and time again that the tool that Google planned as a replacement for cookies—called “Federated Learning of Cohorts, or FLoC, for short—was riddled with privacy problems that even cookies didn’t have. Meanwhile, the way FLoC was designed seemed almost engineered to give Google an even bigger chunk of the digital ad market, when it already controls more of the market than literally any other tech company on Earth.”

Martech: “[The decision]…surely reflects both the confusion among advertisers and publishers confronted by a multitude of alternative identifiers, few of which claim to be able to identify non-logged in users (the vast majority), as well as hurdles facing Google’s proposed alternative, FLoC, including difficulties with European regulators. Many advertisers have rightfully been worried about what the rollout of Google’s privacy initiatives and the blocking of third-party cookies means for their metrics and their clients. This delay means that there is an opportunity for search marketers’ concerns to be heard by the tech giant and that there is more time to prepare for the major changes — including finding technology solutions that adjust when cookies are deprecated, figuring out a first-party data strategy, and pulling data from other sources.”

Rowan Merewood: “It’s time to plan *your own* roadmap for what needs to happen with third-party cookies on your sites and services! In other words… Ask not when third-party cookies will be phased out – ask when you can phase out third-party cookies on your site.”

12

The Real Problem

For the past decade, cookies and various other tracking methods enabled the adtech industry to grow. As our digital lives have grown, the blowback is now coming as the desire for privacy rises. Browsing, apps and emails are all going to get impacted in this privacy-first world. What should digital marketers do? To answer these questions, it is important to look at the real soup that brands have gotten themselves into because of lazy marketing over the past 10-20 years.

Google and Facebook generated $250 billion in revenue in 2020. Where does this money come from? Businesses, spending on targeting past, present and future customers. Let us understand this better.

Because businesses have not built deep relationships with their customers, their customers do not listen to them. Businesses have either not captured adequate data from their customers or do not even know who their customers are. As a result, what do they do? Spend money where the eyeballs are – Google and Facebook. Both have also accumulated plenty of detailed data on individuals thus enabling sharper targeting. Even after the recent changes by Google and Apple, the reality is that the only entities that will emerge stronger are the ones who have the attention, first-party data and targeting technologies – Google and Facebook. Brands seem helpless, but are they really?

Brands attract customers, and then instead of building deeper two-way relationships, they do what? Let many of them go! Best customers are not given differentiated experiences, and others are flooded with generic push messages which get ignored. And then? Brands are back to doing what they know best – spending money with Google and Facebook for new customer acquisition! Little wonder then that Google and Facebook have erected the toll gates on the brand-customer pathway. It is only because brands have let them do it.

At least $100 billion of the money spent by brands on Google and Facebook can be freed up by businesses if they make building direct relationships with their customers a priority. Businesses can invest this money for building better experiences for their Best, rewarding the Rest for their attention, and smarter targeting for the Next.

The key point is this: unless brands prioritise existing customer growth and retention and back it up with a budget reallocation, they will be permanently trapped in the acquisition “doom loop” and always be vulnerable to the changes inflicted by Google and Facebook. The big mistake brands have made is to let these two giants get in between them and their customers. It is time to reclaim the direct relationship and exit the arms race of ever-increasing new customer acquisition costs. This is the key to simplifying marketing.

13

India Adtech and Martech

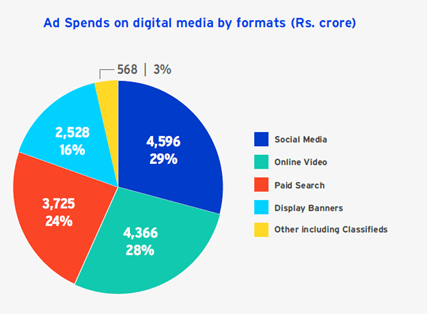

India’s digital advertising market is about Rs 28,000 crore – 35% of the total Rs 80,000 spend, according to Group M’s ‘This Year, Next Year’ (TYNY) report. The charts below from Business Standard based on report provide the full picture:

Denstu’s Digital Advertising report offers a slightly different set of numbers but the broad trends are similar:

Across both these reports, we can estimate the digital advertising spend in India to be about Rs 25,000 crore. Revenues of Google and Facebook in India for the year ended March 2020 were about Rs 18,000 crore, as per Exchange4Media. “Google accounted for lion’s share of digital advertising in India with gross ad sales of Rs 11,442.3 crore in FY20 compared to Rs 9,203 crore in FY19. Facebook has seen a massive jump in its gross ad billing at Rs 6,612.6 crore in FY20 compared to Rs 2,253.7 crore a year ago.” Their duopoly accounts for over 75% of the India digital ad spends and is rising.

Most of this spend is towards performance marketing (primarily new customer acquisition). Startups flush with VC and PE funds, along traditional companies racing to go digital by investing their profits, are fuelling the arms race for new customers.

In contrast, the spend on engagement with existing customers is puny. There are 4 primary digital channels to engage with existing customers: SMS, Email, Push Notifications (PN), WhatsApp. (PNs are not priced on a transaction basis, but come as part of the capabilities offered by martech platforms.)

- SMS: Total spend is about Rs 4,000 crore, of which about 45% (Rs 1800 crore) can be considered as marketing spends. The rest is transactional messaging (15%) and spam (40%). (Unit cost of an SMS is 13 paise, with government entities paying much lower.)

- Email: Total annual spend is about Rs 175 crore. ((Unit cost of an email is about 1-3 paise.)

- Martech platforms: This market is about Rs 500 crore

- WhatsApp: This is still nascent and about Rs 50 crore. (Unit cost of a WhatsApp message is about 30 paise.)

Thus, the aggregate annual spend on martech is about Rs 2,500 crore. This is a tenth of what is spent on digital advertising of Rs 25,000 crore. In other words, brands spend about 10X more on new customer acquisition as compared to engagement with existing customers. (One could quibble over whether the entire digital advertising spend is for acquisition or not, and how much of it is for B2B marketing. Whether the adtech:martech split is 90:10 or 85:15, the fact remains that only a small fraction of the Indian marketer’s budget is spent on customer retention and growth.)

Enlightenment (and change) needs to start with a simple fact that most marketers have forgotten as they have sought to focus on every customer with equal enthusiasm: “All customers are not equal.”

14

Marketing Today

I will begin by first focussing on a brand’s relationship with existing customers and then consider how this can help with new customer acquisition. Let’s first take a look at the current state of digital marketing and engagement.

Most brands (I mean B2C businesses) tend to treat all customers the same; there is one huge bucket into which all customers fall. Segmentation is done more on recent behaviour than on future lifetime value. Some brands use loyalty programs to create tiers and different rewards. “Experience” is spoken of a lot but the reality is quite different; differentiation of experience is the exception rather than the norm. Very few brands take the trouble of getting to know us; they don’t even ask us about our preferences. Martech platforms are used to do the obvious: some standard journeys, the obligatory cart abandonment mail in ecommerce, the bland confirmation when a transaction is done.

The reason for this is that retention and growth is not the exciting part of marketing; it is the stepchild. The darling department is new customer acquisition. That is where the bulk of the budget is spent – the shiny new numbers that can be presented in management review meetings and shown to investors. After all, it is a land grab out there. So why not grab as much territory as possible even if those are deserts, mountains or uninhabited waste land? In fact, to show the infinity of the market, knowingly or knowingly, many customers are re-acquired after being allowed to go dormant.

I had a conversation with a friend recently who had just joined a hot new startup. His traditional market sense was shocked when he saw the spends on acquisitions. VC money was being spent on Google and Facebook to prop up the DAUs and MAUs (daily and monthly active users) so that the next funding round could be at higher valuations. There was little attention being paid to retention. So what if 75% of the app users weren’t even active after a month? There were always new users to acquire to keep the hockey stick curve intact.

With 90% of the monies being spent on acquisition via adtech platforms, very little money is left for customer engagement, retention and growth (the domain of martech). Even this money gets invested in a variety of point solutions – “the next new thing” disease is contagious! The result is that integrating these tech solutions becomes a nightmare and data is siloed. The perfect state of a single customer view never happens. The daily campaigns continue, various numbers are tracked, and whichever looks good are presented to top management. If the going gets tough, it’s time for the marketer to move on – another shiny new startup is waiting with a better compensation package and a bigger acquisition budget.

And so the journeys continue – marketer and customer, the hunter and the hunted, moving ceaselessly, from one brand to another.

15

Customers, Ignored and Ignoring

A brand’s most profitable customers end up with experiences not too dissimilar from the others. We have all experienced it. Except in airlines, hotels and some banks, there is little differentiation in how brands engage with their customers. In the pre-digital days, it was understandable because there was no way to tell one customer from the other – except if a brand had a loyalty program and therefore the points could mirror the customer spend and generate tiers for customers. But in the digital world, this is unforgivable because so much more can be done for creating customer-centric organisations. And yet, click after click, opportunities are lost. The means (acquisition, journeys, campaigns, mailers, notifications, retargeting) overwhelm the end (maximising growth with profitability).

The most profitable customers do not get differentiated experiences and hence can be tempted away, ending up as an increase in the “churn” column of the marketer. At best, there is a transaction-based loyalty program with tiers to retain them. Points are stored in a black hole and redemption is made almost impossible. At some stage, customers even forget they have some points and soon end up forgetting about loyalty also. All that still holds them back is a mix of habit and inertia.

The rest of the customers are less attached to the brand. They were in a relationship once with the brand, but the lack of friendly engagement distances them from the marketer. A little signal here, some TLC there, and who knows what love could have blossomed. But alas, it was not to be. No attempt was made to make them feel welcome, no effort was spent on asking what they liked. Instead, all they got was the same stream of messages day after day. And at some point, they stopped opening the mails, clicking on the SMSes, actioning the notifications – and no one even noticed. A performance statistic declined by a few basis points, perhaps they were the third or fourth decimal after the point.

They drift away – and guess what! They get targeted for re-acquisition after some time. They are now in the vast pool of “new customers” – meaning more money can now be spent on them to bring them back into the fold. The irony is not lost. Thinks the customer, “I was once yours. We went out for a date. I could have fallen in love. But you were too busy, with all your data and dashboards. I waited and waited for the right move and message. I kept signalling you – by not opening your messages. It didn’t matter. I left. It still didn’t matter.” And now the marketer is back to paying Google and Facebook – paying for attention that was once available for free.

And so the cycle of life continues. Acquire, lose, re-acquire, lose, re-re-acquire. A vicious spending loop in the ever-increasing new customer acquisition budget. Thinks the customer, “Only if you had taught me to not ignore you, we could have both lived together, happily ever after.”

16

Anyone Listening?

Ajay Row had this to say in a LinkedIn post about the cost of inattention:

You are a smart marketer with a 10% open rate on your emails and a 20% click-through rate, so effectively 2% (10% x 20%) of your audience respond to you in our (overly-simplistic) example.

Let’s understand this.

First, your 10% open rate means you have a 90% non-open rate — which means 90% of your database ignored you. For these folks, nothing bad happened. Life did not dramatically change for the worse. So they have been taught that ignoring you has no downside. So they will continue to ignore you, and keep getting reassured afresh with every email they ignore, till your emails no longer even register in their brains, become a blind spot and with that, eventually, your brand in the Inbox. Until of course an ever-helpful inbox prompts the customer to unsubscribe, and they do, never to feel the loss.

Now to the 10% who do open your emails. Lovely people. Bless them. Let’s say your CTA is really cool and 20% (!) click on it and the remaining 80% delete your email without clicking. Which means 80% of 10% (8%, we are now at 98% of your customer base and counting) have been educated that to open your email is a mistake. Some, optimists, will open more emails, others have learned to ignore you. Optimism is a rapidly degenerating function in the email world though.

The worst part, last. The 20% of the 10% (2% in all) who clicked on your link, all eager to move ahead. Let’s say you have not figured out your landing page strategy (I know we said you are smart but even the smartest don’t think through the post CTA journey sometimes) and 80% of these folks are unable to do whatever it is that you want them to do and they want to do. Ouch! They rapidly join the ranks of the “let’s ignore this smart marketers’ brand”; except, with a vengeance.

This cost is not measured on a P&L and hence does not total into a balance sheet. But to my mind it is a real cost of incompetent and uncaring marketing that impacts a brand and its ability to communicate with its customers.

And think: what if a significant portion of a brand’s more valuable customers are ignoring it? This is revenue loss that brands don’t even factor in.

Attention must become the new Acquisition. Without attention, there is no engagement. Without engagement, there is no transaction. In the trees of continuous new customer acquisition, brands and marketers have lost the joy of the forest of customer attention, delight, and engagement. It is time to go back to the basics. It is time to simplify marketing. But to do that, we have to first understand the big idea that marketing has largely missed.

17

Power Law

Marketers for the most part have missed the “power law of marketing” – that a relatively small percentage of customers account for a big chunk of revenues and make an even bigger contribution to profits. For many non-subscription brands, an analysis based on customer lifetime value (or even past transactions) will show that 20% of the customers contribute 60% of revenues and more than 100% of profits. What this also means is that 80% of the customers contribute 40% of revenues and are a net cost to the brand if one factors in acquisition and servicing costs.

The power law of marketing (which can also be interpreted as the 80-20 rule or the Pareto principle) is core to the idea of simplifying marketing. I have discussed this in a previous blog series The One Number to Predict Revenue. Here is how it looks:

The X-axis sorts customers while the Y-axis is the CLV. The area under the curve is the net predicted revenue – the aggregation of the CLV of each customer. The Best customers are towards the left of the X-axis (their revenue represented by the green shading) while the Rest customers make up the long tail (their revenue represented by the yellow shading). As I explain in my series, power laws are all around us. Most marketers have not opened their eyes and seen their customers in this context.

The complexity in marketing has arisen because of a lack of understanding of the fact that all customers are not equal and some are more valuable than others. By not differentiating between the Best (top 20%) and Rest (remaining 80%) customers, marketers have complicated their own lives – having to focus on a much larger base than they actually need to. Instead of providing amazing experiences for the most profitable customers, marketers have gone down the path of trying to provide a “lowest common denominator” experience to their entire base. This is ineffective and results in the churn of the Best and continuous re-acquisition of the Rest. No one is happy with the outcome.

What marketers need to do is to actually create two internal business units to focus on the Best and Rest customers. Their needs are different, the approaches to be followed are different. The same team cannot address the top 1% and the bottom 1%. And yet, I have not seen brands do this – outside of a few industries like airlines where a single transaction itself enables the segmentation and experience differentiation.

The reason for this is that most marketers do not think about customer lifetime value (CLV). Ironically, marketers are awash in customer data and the CLV calculation and identification of Best Customers is much easier now that it ever was. Marketers tend to think of the more immediate past (which customers have been active in the past 30/60/90 days) rather than analysing the long past (2-3 years) to predict the near future. The right CLV model needs to be used to factor in recency and frequency to calculate CLV for each customer and then segment them into Best and Rest. Without bringing in CLV and just looking at transactions from a narrow lens, all customers will look the same. As a result the focus ends up becoming on the trees (campaigns) rather than the forest (experience).

The power law of marketing is the big foundation idea for simplifying marketing. Understanding that the 20% Best Customers are many times more valuable than the 80% Rest Customers is the big insight that can remake marketing.

18

Money on the Table

Let’s dig deeper into the impact of the power law of marketing.

We can segment customers into Best (top 20%) and Rest (remaining 80%). Another way is to think of them as High, Medium and Low value customers – H, M, L. The following calculations are very simplistic but they will make the point that marketers are leaving a lot of money on the table by not getting customers to pay attention to their marketing messages.

- Top 20% customers [H] = 60% revenue; average for each 1% = 3%

- Next 30% customers [M] = 20% revenue; average = 0.67%

- Bottom 50% customers [L] = 20% revenue; average = 0.4%

Now, let’s assume that with better marketing, revenues from H and M customers can be increased.

- Revenue from H customers increased by 10% = 60 à 66 units

- Revenue from M customers increased by 20% = 20 à 24 units

This will lead to a total revenue increases by 10%. The marginal costs will not increase substantially and much of the extra gross margin will flow straight to the bottom line resulting in an increase in profits by at least 25-30%.

If marketers can play the attention game right, the impact can be even greater. This is the money marketers are leaving behind. Therefore, it is critical for marketers to get customers, especially H and M, to pay attention to their messages.

But as we all have experienced, this does not happen. Here is the reality of attention:

- Emails: open rates 5-15%

- SMS: open rates 10%

- PNs: blocked / undelivered to ~50% of base

The net result is that a very large majority of customers are ignoring incoming messages. What if most of these are H and M customers? Have marketers done a correlation between CLV and engagement? If a brand’s valuable customers can be persuaded to open more messages, can that lead to more transactions? These are the questions that marketers should be asking – rather than figuring our whether they should be spending more on Google or Facebook!

To ensure “No Money Left Behind”, marketers need to work on the following:

- Get H and M customers to pay attention

- Else they are leaving a lot of money on the table (for competition)

- Change customer mindset from delete to delight

- How to train customers to never ignore messages?

- How will they buy if they don’t know what is on offer?

- Convert 1-off engagement into continuous relationship

- Make opening and acting on messages a habit

- Segment customers based on value

- H (Best) more valuable than M who are more valuable than L

- Selectively incentivise customers for specific actions

- Do all this without any new budgetary allocation

This is marketing’s greatest challenge – and opportunity. And the simple truth that marketers have missed is: “To get customers to pay attention, pay for attention.” In fact, marketers know this very well – they are just paying the wrong entities for attention. It is time they stopped fattening the profits of Google and Facebook, and instead consider a rewards program to incentivise their existing customers for attention and action, the upstream of transactions. This is the secret to ensuring there is no money left on the table – for competition. The next question: what do marketers have to do differently to win their customers’ attention?

19

Building Blocks

Marketers need to start thinking like CEOs – or at least like Chief Profitability Officers for the business. Their goal is not to optimise campaigns and journeys, but to drive business growth. To make this happen, marketers need an Attention Stack. The starting point is to understand who the Best Customers are and what’s common to them. The three building blocks for this are customer data platform (CDP), customer lifetime value (CLV) and Best Customer Genome (BCG).

The CDP is the repository of all customer data across all touchpoints. In the non-digital world, customer data was very hard to collect – this is why retail stores introduced physical cards which shoppers could scan at checkout allowing the store to connect customers to their buying behaviour. In the digital world, this is much easier: all actions done on the website or app can be captured and stored in a database. I have discussed the CDP in my How Velvet Rope Marketing can transform Customer Loyalty series.

As defined by the CDP Institute, “A Customer Data Platform is packaged software that creates a persistent, unified customer database that is accessible to other systems…The CDP creates a comprehensive view of each customer by capturing data from multiple systems, linking information related to the same customer, and storing the information to track behavior over time. The CDP contains personal identifiers used to target marketing messages and track individual-level marketing results.” More from the Hubspot blog: “CDPs build customer profiles by integrating data from a variety of first-, second-, and third-party sources. This includes your CRM and DMP, transactional systems, web forms, email and social media activity, website and e-commerce behavioral data, and more.”

With the data in a single store, it becomes possible to calculate CLV for every customer and decode the BCG.

As I wrote previously in the Velvet Rope Marketing series quoting Peter Fader: “CLV is a forward-looking, predictive measurement that is calculated by modelling and projecting the following: how long the customer relationship lasted (for churned customers) or is likely to last (for active and future customers), number of transactions, value of the transactions, and other non-financial activities the customer may engage in. Eg. visits to website, willingness to try other products, posting ratings and reviews about the company’s products, and/or referring other prospective customers.”

I also explained BCG in the Becoming Chief Profitability Officer series: “The Customer Genome provides a distinctive digitally encoded representation of a customer. It allows us to compare different customers, predict what a specific customer is likely to do next and create personalised experiences… By looking at the Customer Genomes of the Best Customers as determined by their CLV, it now becomes possible to identify the Best Customer Genome (BCG) – those attributes and actions common to the most valuable customers of a brand… Knowing how these customers are different lets us replicate their attributes in acquisition and behaviour in the onboarding process to ensure that brands can manufacture more Best Customers.”

With this foundation in place, it becomes possible to focus on the business outcomes.

20

Profipoly

If we were told to design the ideal business with no resource constraints, what would we do?

The goal would be to maximise industry profits, thus leaving no surpluses (“oxygen”) for competition to invest and grow. As we have seen, not all customers are profitable if acquisition and servicing costs are factored in. So, the first task would be to identify the sector’s most profitable customers and acquire them.

Once acquired, the next objective would be to ensure to keep them forever and get 100% of their spend in that category. This would necessarily mean providing them with the best possible experiences (“velvet rope marketing”) and perhaps combined with a loyalty program that keeps the goodies coming as they keep spending. Airlines do this amazingly well with their loyalty programs. The “loyalty lock-in” ensures that travellers want to stick to the same airline, accumulate miles, move up the tiers, and get rewarded with better experiences. The perfect business would do the same – design experiences to ensure customers never churn and maximise their spend with the business.

The next stage would be to turn customers into advocates – thus dramatically reducing acquisition costs for the Next (Best) customers. Best customers are likely to know other potential Best customers in their friends and family network. Incentivising them to get more like them can create a continuous supply of new customers with similar characteristics in terms of spending and profitability. Once a new customer is acquired, the business then has to accelerate that customer’s journey to profitability by enabling them to follow in the footsteps of the Best customers – this is where the Best Customer Genome comes in by suggesting what products or services to recommend at each stage of the customer journey.

If all of this can be made into a repeatable process, the flywheel kicks in – and that’s the secret to super-normal growth and profits. It is what the best businesses do. Look at Amazon and Costco and you will see this growth flywheel at work. Amazon Prime and Costco’s Membership program are the cornerstones of building businesses that suck out the oxygen of growth from competition and create a “profits monopoly” (profipoly).

As I wrote previously in Best Customers and Velvet Rope Marketing: “By building a double moat of getting the industry’s Best Customers and then maximising revenues from them, it becomes possible to create a profits monopoly (profipoly) which can cut off the oxygen that competition needs to grow.”

This brings us to the next set of questions: How does one create such a business? How can the marketer help in designing such a business? What impact will all the recent privacy-linked changes by Google and Apple have on the design? Is marketing really that simple? If so, why isn’t everyone doing it this way? How can marketers get started on this journey?

21

Three Teams

At its simplest level to get as close to the ideal, businesses (and marketers) need to do three things: keep the Best customers forever, migrate the Rest customers to becoming Best, and acquire Next customers with the potential to become the Best. In other words: Retain the Best, Rest to Best and Next like Best. Each of these three functions are distinct and need to be run by different teams for Best, Rest and Next customers.

Best: The goal of this team is to imagine the most amazing experiences for the top 20% customers. While they view the brand positively and don’t need much prompting to return to the brand’s properties, the question marketers must ask is: how can one go beyond just loyalty programs and treat these customers like royalty? This is where the ideas of “Velvet Rope Marketing” come in. Exclusivity, ease and access are three axes to define new customer experiences. Further reading:

- Velvet Rope Marketing

- Becoming Chief Profitability Officer

- The One Number to Predict Profits

- Rethinking Referral Marketing

- How Velvet Rope Marketing can transform Customer Loyalty

- Best Customers and Velvet Rope Marketing

Rest: For the other 80%, the number one challenge is to get engagement going with the marketing messages being sent by the brand. These customers are not yet loyal to the brand and tend to ignore the emails, push notifications and SMSes sent. Brands have limited data about them thus making it difficult to do segmentation and personalisation. Without actions on the messages, it is very difficult to bring the Rest customers to the brand properties. And without them visiting the website or opening the app, it is almost impossible to get them to do transactions. Also, loyalty programs (in case they exist) don’t work with them because they never earn enough points to garner the rewards and benefits. So, the key challenge is to ensure the Rest customers engage with brand communications. Push messages are the only way to reach out to the Rest. They need to be lured back. This is where the ideas of Microns and Mu come in – to get customers to pay attention, pay for attention. Think of this as “Attention Rewards Marketing” (ARM) – messages with goodies to begin a lifelong relationship with customers. This is the starting point for migrating Rest to Best. Further reading:

- Microns: Making B2C Emails Better

- Microns: Theory and Economics

- Microns and Brands: Made for Each Other

- Micron-verse: The New World of Brand-Customer Communications

- Microns: Solving the Customer Reactivation Problem

- Microns and AMP: A Powerful Combo

- Microns and Loyalty: Gamifying and Rewarding Attention

- Micronbox: A New Inbox

- Imagining Mus: An Attention-Action Currency

- Micron-verse: Making It Happen

Next: Brands have been focused on new customer acquisition since time immemorial. The only change that needs to be done here is to acquire new customers based on the Best Customer Genome (BCG) rather than indiscriminately. Instead of relying on only Google and Facebook, brands should persuade their Best customers to refer others like them – and that is only going to happen when the Best customers have experiences they can talk about and share on their social networks. Each Best customer is a micro-influencer. This is the best way to acquire Next like the Best. This team thus needs to focus on cloning the attributes and behaviour of the Best for new acquisition and onboarding.

Three teams, each with clear objectives: protect the Best, persuade the Rest, prospect the Next. One common theme: get existing customers to pay for attention. How can marketers make it happen?

22

Pay for Attention

One of my earliest memories (as a kid in the 1970s) of a loyalty program is collecting Ramon Bonus stamps. After that, if my memory serves me right, I collected stamps from Akbarally’s from purchases made at their Fountain store in Mumbai. Both were early examples of programs that rewarded loyalty. In the past 50 or so years, we have seen an explosion of loyalty programs. All of these programs reward transactions. But none reward the two elements that are upstream of a transaction – attention and action.

For marketers to engage with their customers, attention and action are very important. As I wrote earlier, both are upstream of transactions. In the digital world, because every customer has a uniquely addressable identity (email ID or mobile number), it becomes possible to interact with each of them. If the brand imagery or habit doesn’t bring a customer back to a brand’s properties, the only other route is via push messages – sent by SMS, email, push notifications (on apps) or WhatsApp. For these messages to be effective, customers need to ‘pay attention.’

As we saw earlier, the sheer volume of incoming messages flooding the inboxes of customers has resulted in them (all of us) ignoring most such messages. The result is that this breaks the communications hotline for marketers – forcing them to resort to very expensive ads via Google and Facebook to win back the attention they have lost of the customers who were once theirs.

It is in this context that I have discussed the idea of Microns and Mu. Microns are messages with rewards, with Mu being the virtual currency that incentivises attention and action.

Microns delivered as email have additional benefits: they improve the reach and deliverability of email, thus solving two additional problems most email marketing programs face.

Microns and Mu are just one example of rewarding customers for their attention. The key is to remember the point I had made earlier: “To get customers to pay attention, pay for attention.” And the payment (in the form of rewards) should be made directly to customers. This innovation can go a long way in simplifying marketing by solidifying the relationship between brands and customers, which is what it should always have been.

By combining VRM (Velvet Rope Marketing) for Best customers and ARM (Attention Rewards Marketing), marketers can go a long way in correcting their folly of solely relying on intermediaries (media platforms, tech giants, and increasingly, marketplaces) and build 1:1 relationships with their customers.

23

Making It Happen

The success of the new marketing ideas will be dependent on the budgetary allocations. In most brands today, the Best:Rest:Next budget is 2:8:90. The largest chunk is for new customer acquisition. A small allocation is for existing customers and since there is no differentiation, the spends in the Best and Rest category end up being proportional to the customers in these segments. In fact, most brands do not even have a Best and Rest split – treating them just as a single bucket of “All Customers”.

The right way to allocate budgets is to allocate equally to all the three segments. While this may not happen immediately, a starting point should be to make the allocation 20:20:60 – reduce the acquisition budget from 90% to 60% and then spend the remaining budget equally for Best and Rest customers. Only when brands follow their customers and reallocate their money will this new simplified marketing approach.

Where should marketers spend this new money for Best and Rest customers? The short answer is: the marketing cloud. But how?

First, marketers need to get the ABC right – Analytics, BCG and CLV. CLV is key for customer segmentation and correctly identifying the Best customers. BCG tells marketers more about the attributes and activities of the Best customers – this is what has to be cloned for everyone else. Analytics and AI-ML can help make this process simpler – with continuous learning.

Second, marketers need a customer communications, engagement, and experience (C2E2) stack. This stack forms the core tech for Velvet Rope Marketing and needs to be activated only for the Best customers. While point solutions can be bought and integrated together, a full stack solution is likely to work better because it will eliminate the tech connectivity and data sharing challenges. More importantly, with all the data in a single store (rather than multiple silos), the magic of AI-ML can work much better. What the marketer needs is to know what happened yesterday, what to do today (next best action), and what is likely to happen tomorrow – a good AI-ML engine will help with the analytics and predictions freeing the marketer from the tyranny of the daily routine.

Third, marketers need M3 (Messages-Microns-Mu). Push messages need to be transformed into microns with rewards (Mu). These messages offer incentivises for attention and action for the Rest so they never ignore brand communications. It is better to pay one’s own customers for their attention rather than compete in auctions on Google and Facebook and spend 10 times more money in re-acquiring them via ad platforms.

Finally, marketers need an Adtech-Martech Bridge (AMB). This bridge serves two purposes: prepare the right attributes and profiles for adtech platform for acquiring the Next customers (lookalikes of the Best), and ensuring that the onboarding process is smooth for these first-time customers. So far, adtech and martech have largely operated independently even though they target the same customers at different points in the journey. The AMB is the missing link which can further optimise ad spend budgets.

Much like Luke Skywalker had R2-D2 and C-3PO, the modern marketer needs ABC, C2E2, M3 and AMB. And to all such marketers willing to make the leap, “May the Force be with You.” And as Qui-Gon Jinn says, “Your focus determines your reality.”

24

The Constellation

Bringing to life the world of ABC (Analytics, BCG and CLV), C2E2 (Customer Communications, Engagement, and Experience), M3 (Messages-Microns-Mu) and AMB (Adtech-Martech Bridge) is beyond what a single company can do. What it needs is a collective – a constellation.

In astronomy, a constellation is a group of stars that forms a pattern in the night sky. As Wikipedia puts it, a constellation is a “recognisable pattern of stars whose appearance is associated with mythological characters or creatures, earthbound animals, or objects.” Examples of constellations include: The Big Dipper/Ursa Major (‘The Great Bear’), The Little Dipper/Ursa Minor (‘The Little Bear’), Orion (‘The Hunter’), Taurus (‘The Bull’) and Gemini (‘The Twins’).

In businesses, a word that as used in the context of Japanese companies was keiretsu. According to Investopedia, “Keiretsu is a Japanese term referring to a business network made up of different companies, including manufacturers, supply chain partners, distributors, and occasionally financiers. They work together, have close relationships, and sometimes take small equity stakes in each other, all the while remaining operationally independent. Translated literally, keiretsu means “headless combine.” Examples of keiretsu groups include Mitsubishi, Mitsui, Sumitomo and Sanwa.

In global business, two words that have become common are platform and ecosystem. Almost every company likes to use one of these to define what they are doing. I prefer the word “constellation” – to define a group of companies that work together to solve problems none can solve on its own.

At Netcore, we have been working to build such a constellation of companies. Two partners are EasyRewardz and ProfitWheel. Together, this trio can help implement the many ideas we have discussed here.

ABC: Netcore and EasyRewardz can help do this for online and offline companies. The goal is to aggregate data from all touchpoints into a CDP, and then use CLV to segment customers and identify the brand’s Best Customers. These are customers who need Velvet Rope Marketing – a way to create differentiated experiences so that they never churn and maximise their category spend with the brand.

C2E2: This is what Netcore has been focused on for many years.

EasyRewardz too has significant capabilities in customer lifecycle management. As the Netcore press release about its investment in EasyRewardz put it, “With this strategic investment, Netcore Cloud can now do a tighter integration with the Easyrewardz platform and offer the CLM stack to its customers, across all the touchpoints, building on their promise of Omnichannel Intelligent Customer Experience… Leveraging deep integration of the platforms from Netcore and Easyrewardz, we are excited to bring to our clients, a true omni-channel marketing automation suite, integrated with POS that offers real-time rewarding capabilities across points, coupons and vouchers, and experience assessment via feedback, survey or polls.”

M3: This is a new idea that we have been working on at Netcore.

Mu can be integrated into any push messaging channel by any brand, instantly creating a rewards mechanism for attention and desired action, as precursors to transactions.

AMB: This is where ProfitWheel comes in. By taking data from martech platforms, it can improve new customer acquisition to focus on those customers who have the attributes of the Best. Data about new customers can also be used to improve the onboarding experience for future Best customers.