Published August 13-20, 2021

1

India

In the late 1990s when I was running IndiaWorld, I remember eagerly reviewing prospectuses of Internet companies that went public. The documents were rich with information about the business models and had a lot of numbers about the nascent and emerging digital industries. Prospectuses then were hard to come by, so I would use visits to investment banks to pick them up, along with the analyst reports which distilled the thick documents into readable summaries.

As the era of Internet IPOs begins in India (a decade or two delayed), the filings by companies going public in the form of the DHRP (Draft Red Herring Prospectus) offer a similar treasure trove of information. In this series, I will aggregate the important information from these documents so it becomes a useful ready reference. While much of it may be available elsewhere, having it all available in a single place can be useful and helpful. I have used various DHRPs downloaded from the Sebi site.

Every DHRP starts with the India big picture:

- GDP growing from $2.9 trillion in 2019 to $4.4 trillion in 2025 with a CAGR of 7.2% – Zomato

- 6% population in the age bracket of 20-59 years – Zomato

- India has 745 million people in the working age group as compared to 172 million in US and 849 million in China. India is one of the youngest nations in the world, with a median age of 28 compared to 38 in China and the United States, 43 in Western Europe, and 48 in Japan. India has 700 million generation Z and millennials, largest in the world. – Paytm

- Indian middle class is 55-57% of the population currently, and is likely to be 65%+ of population by 2030 – Patym

- Private consumption is expected to increase from US$ 1.6 trillion in 2019 to US$ 2-2.5 trillion in 2025 – Paytm

India’s demographics, from MobiKwik:

Nykaa highlights the “Young India” opportunity:

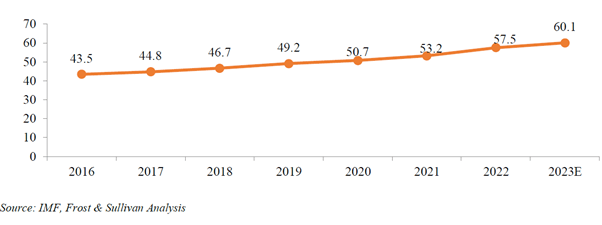

Nazara shows the per capita national income…

… and the growth in per capita personal income (in thousands of rupees):

2

eIndia

The numbers about India’s Internet and smartphone penetration:

- Internet: 570-600 million (2019), going to 950-1000 million (2025) – Zomato

- Smartphone: 33% penetration (2019), going to 58% by 2025 – Zomato

- Active Internet users: 400-430 million (2019) – Zomato

- Online service users: 220-250 million (2019) – Zomato

- Online shoppers: 120-150 million (2019) – Zomato

- Social media users: 300-350 million average monthly active users in 2020 across platforms like Facebook, Youtube and Instagram – Nykaa

A chart from Patym has similar data about the top of the funnel:

More from Policybazaar:

This chart shows a sharper comparison with China:

Another view of the India-China comparison from Nykaa, and a view of India in 2025 comparing favourably in absolute numbers with China in 2020:

As we can see, China is at 4X of India in online shoppers. Given that China’s per capita GDP is 5X of India ($10,000 vs $2,000), this gives a 20X differential in spending potential in China vs India. This shows up clearly in the analysis of the food delivery market:

At $90 billion China’s online food delivery market is almost 22X of India’s $4.2 billion, as per Zomato’s estimate based on 2019 data.

MobiKwik’s estimates offer a broader definition of online transactors:

The difference between transactors and shoppers is highlighted below by Mobikwik:

3

Digital Payments

Policybazaar offers the big picture:

Additional info via Paytm:

And this on household debt as % of GDP, which shows China at 5X and the US as 7X of India.

Fino offers an overview of the various players using digital medium across different financial segments:

A chart from Paytm shows the exponential growth in digital payments:

More from Fino on the rise of digital payments (above was in dollars, below is in Indian rupees)…

… and retail payments:

Mobile payments expected to reach ~ US$ 3.1 trillion by value by FY 2026rising 5X from 2021, as per Paytm. The digital payments funnel looks like this:

Some additional data points:

- 65 million merchants of which 45 million have access to internet – Paytm

- 30-35 million unique merchants are using QR codes for digital payments in India and expected to increase to 55-60 million by FY 2026 – Paytm

More data from Paytm:

- Total outstanding loans in India expected to double to $1 trillion to 2026 from $550 billion in 2021

- BNPL (buy now pay later) is expected to grow 5-6X to $90-100 billion by 2026

- MSME loans expected to grow from $375 billion in 2021 to $600 billion in 2026

One of the reasons for the digital opportunity is because of the low penetration of bank branches and ATMs in India, as detailed by Fino:

An additional insight from Fino: In India, there were 4.7 million PoS terminals and 0.24 million ATMs deployed across the country as on March 31, 2021. ATMs and PoS terminals have grown at a CAGR of 4% and 28%, respectively over the past five years.

4

Insurance and Healthcare

The Insurance big picture comes from Policybazaar:

Insurance penetration, as per Paytm:

An additional pointer from MobiKwik: In 2019, the penetration of insurance, life insurance and non-life insurance in India was 3.76%, 2.82% and 0.94%, respectively, which is relatively lower in comparison to the global penetration of insurance, life insurance and non-life insurance of 7.23%, 3.35% and 3.88%, respectively.

On healthcare, Policybazaar offers this:

5

Consumer Lending

A perspective on consumer lending from Policybazaar:

The next few charts show the current state and future prospects for personal loans, credit card loans and housing credit in India:

An interesting sidelight about the business model of credit card companies from SBI Cards:

6

Stock Market, Mobile Wallets, BNPL

An overview of stock market and mutual fund participation, as per Paytm:

In 2020, the mutual fund investor penetration in India was approximately 2% in Fiscal 2021 with the AUM to GDP ratio at approximately 16% as compared to approximately 145% for the United States, as per MobiKwik.

Mobile wallets data is offered by MobiKwik:

The rise of BNPL (buy now pay later), as suggested by MobiKwik:

The BNPL opportunity arises in part because of the low credit card penetration in India as MobiKwik’s data shows:

7

Retail India

The big picture from Fino Payments Bank: “the private final consumption expenditure (PFCE) was 58% of GDP in financial year 2021 at ₹ 116 trillion and India’s retail spending on goods was at ~50% of its private consumption.”

Fino adds: India retail spending is projected to touch ₹ 91 trillion by financial year 2025, with smaller stores and organised retail to co-exist.

Nykaa offers a deep dive into the growth:

Organised retail in India, which accounted for 15% of the retail market in 2019 (4% up from the share in 2016), as per Nykaa.

The changing Indian is showcased in this chart from CarTrade:

The pandemic-fuelled growth in ecommerce is highlighted by MobiKwik:

The digital commerce opportunity in India, as highlighted by Patym:

Nykaa offers some interesting insights into India’s beauty and fashion markets:

Nazara highlights the gaming opportunity in India:

8

Looking Ahead

India’s moment in the Internet world has finally arrived. Zomato’s IPO and its heady valuation is going to be the start of a flurry of listings in the coming months. Investment banks are racing to use estimates many years hence (one even went up to 2031) to justify the current stock prices. What the right valuation and price should be for Internet companies will be hotly debated topics. What’s clear is that the new-age companies, powered by tech, have plenty of headroom for growth. The key to sustaining investor expectations will be crafting a path to profitability. Spends on new customer acquisition can drive growth but only customer retention and maximising revenue from each of them will ensure sustained profits.

A word of caution about India’s Internet numbers was sounded recently by The Ken’s Nutgraf. It estimated India’s annual active Internet customers to be at 70 million, split thus: 10 million at the highest level (digital natives), 20 million occasional shoppers, and 40 million entry shoppers.

Of course, the companies getting listed and the VCs and PEs investing hundreds of millions weekly into India’s digital ecosystem have a different view. With hundreds of millions of future customers, young and eager to spend, a new world beckons. The disposable income of Indians is increasing with economic growth, the number of digital users is increasing, and the options and ease of digital spending is growing. Everything not digital is getting disrupted – from payments to banks, from education to health, from shopping to entertainment. A new future beckons, and investors bet on big winners. And there will be many. Along with B2B SaaS, India’s digital ecosystem offers the next trillion dollar opportunity.

The golden age of Indian entrepreneurs has begun. This is now irreversible. Investor funds by the hundreds of millions are creating unicorns aplenty. With acquisitions and IPOs, this nominal wealth is getting converted into real money. This will find its way to new entrepreneurs as startup capital. Many will fail, but that’s the nature of the game. The winners will be big and that drives dreams for everyone else. These entrepreneurs will help make a better India – solving problems created through the decades by India’s government with its licence-permit-quota-raj. Risk capital was always a challenge in India and that is now getting solved. As long as India’s government doesn’t mess it up (and they cannot make things better) and let the markets work, India’s slow steps to prosperity will start. The initial beneficiaries will be those at the top of the pyramid, but it will percolate down to all in the decade to come. As the startup and digital boom is showing, what Indians need is economic freedom. The only risk to this new future is someone in government wanting to help!